Protection from Storm Damage

Mitigating your home against severe weather can keep your family safe as well as save you money. All Florida Home Insurers are required to offer discounts to homeowners who add these features or use specific home construction techniques.

According to the Florida Division of Emergency Management, 15% – 70% of home insurance premiums in Florida can be attributed to wind-damage risk. While there is an upfront cost involved, outfitting your home with wind mitigation features can result in significant long-term savings.

| Wind Mitigation Feature | Hypothetical Estimated Premium Savings Example Based on mitigated hurricane-wind premium of $1,518, part of a total premium of $3,704.* |

|---|---|

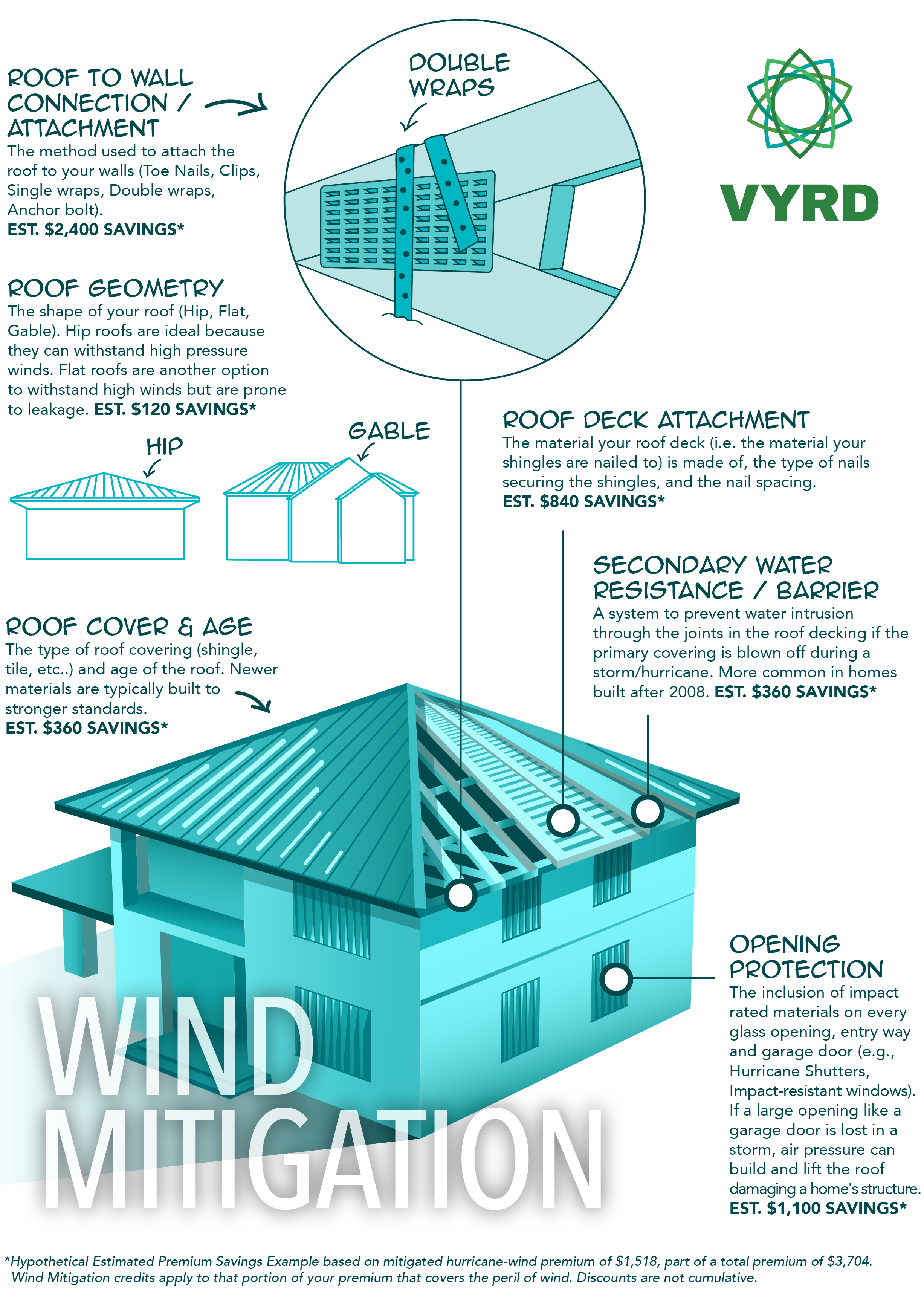

| Roof Age: the type of roof covering (shingle, tile, etc..) and age of the roof. Newer materials are typically built to stronger standards. | Roof Covers meeting the Florida Building Code reduces the hurricane portion of the premium approximately $360 |

| Roof Deck Attachment: the material your roof deck (i.e. the material your shingles are nailed to) is made of, the type of nails securing the shingles, and how far apart the nails are. | Roof deck attachments based on the most stringent nail size and spacing code requirements reduces the hurricane portion of the premium approximately $840 |

| Roof Wall Connection / Attachment: the method used to attach the roof to your walls (Toe Nails, Clips, Single wraps, Double wraps, Anchor bolt, …). Double wraps are considered the strongest. | Roof wall connection consisting of double wraps reduces the hurricane portion of the premium approximately $2,400 |

| Opening Protection: the inclusion of impact rated materials on every glass opening, entry way and garage door (e.g., Hurricane Shutters, Impact-resistant windows). If a large opening like a garage door is lost in a storm, air pressure can build and lift the roof damaging a home's structure. | Installation of building code compliant hurricane shutters reduces the hurricane portion of the premium approximately $1,100 |

| Roof Geometry: the shape of your roof (Hip, Flat, Gable). Hip roofs are ideal because they can withstand high pressure winds. Flat roofs are another option to withstand high winds but are prone to leakage. | Hip Roof savings versus gable roof reduces the hurricane portion of the premium approximately $120 (note, Hip Roof savings can vary substantially based on risk location, year built, other wind mit features) |

| Secondary Water Resistance / Barrier: a system to prevent water intrusion through the joints in the roof decking if the primary covering is blown off during a storm/hurricane. More common in homes built after 2008. | The addition of Secondary Water Resistance reduces the hurricane portion of the premium approximately $360 |

Curious about how much you could save if you have these mitigating features on your home?

Be sure to review the Notice of Premium Discounts for Notice of Premium Discounts’ for Hurricane Loss Mitigation (OIR-B1-1655). You can find this form attached to your Homeowners Insurance policy. By examining this form, you’ll get a clear picture of the savings you can enjoy, helping you make informed decisions.

Wind Mitigation Inspection

Generally, a wind mitigation inspection is needed to determine which credits apply to your home. It starts with hiring a certified inspector. That individual maybe a contractor, architect, engineer, or a home inspector and they look for these key features and add-ons in your home.

Inspections typically cost about $150 (depending on where you live) and take 30 minutes to an hour.

VYRD can provide you with contact information for third-party wind mitigation inspectors. Call us today at 888-806-VYRD (8973), work with your Agent or find a local VYRD Agent.

You may also be able to take advantage of the My Safe Florida Home program administered by the Florida Department of Financial services. It provides qualifying homeowners with free wind mitigation home inspections and awards wind mitigation grants to go toward storm hardening homes.

Once the inspection is complete, you receive a wind inspection report. In that report, the inspector will offer suggestions that could improve the sustainability of your property. The costs of these improvement projects will vary and VYRD recommends that Homeowners contact a licensed contractor for an estimate. You can find a Certified Contractor in your area by visiting the Florida Department of Business and Professional Regulation.

*Wind Mitigation credits apply to that portion of your premium that covers the peril of wind. Discounts are not cumulative.